All the Questions You Want Answered About Transferable Tax Credits

Written By: Kim Spurgeon, Director of Film Nevada

What are transferable tax credits?

In simple terms, a tax credit is a reduction in the amount of taxes owed. For example, if a business owes $1,000,000 in taxes and has a tax credit of $250,000, it could apply the tax credit to their tax bill and only pay the remaining $750,000. A transferable tax credit can be transferred from the entity that earned the credit to another entity to apply toward their taxes. For Nevada’s Transferable Tax Credits for Film and Other Productions program, that means a production company eligible to earn credits can transfer them to another Nevada business with certain tax liability.

How does the film tax incentive program work?

The program is used as a tool to attract productions, including films, television series, game shows, commercials and more, to film in Nevada that may have otherwise filmed elsewhere. These productions hire local Nevada residents, spend money with local Nevada businesses, and showcase Nevada locations on screens big and small.

The program, funded at $10 million annually, offers a 15% transferable tax credit to productions spending at least $500,000 and 60% of their total budget on qualified costs in Nevada. The tax credit rate can increase if any bonuses are achieved. An additional 5% can be awarded if a production hires at least 50% of below-the-line crew as Nevada residents, and another 5% bonus is available to productions filming at least 50% of their shoot days in a qualified rural county. The maximum tax credit a production can earn is $6,000,000.

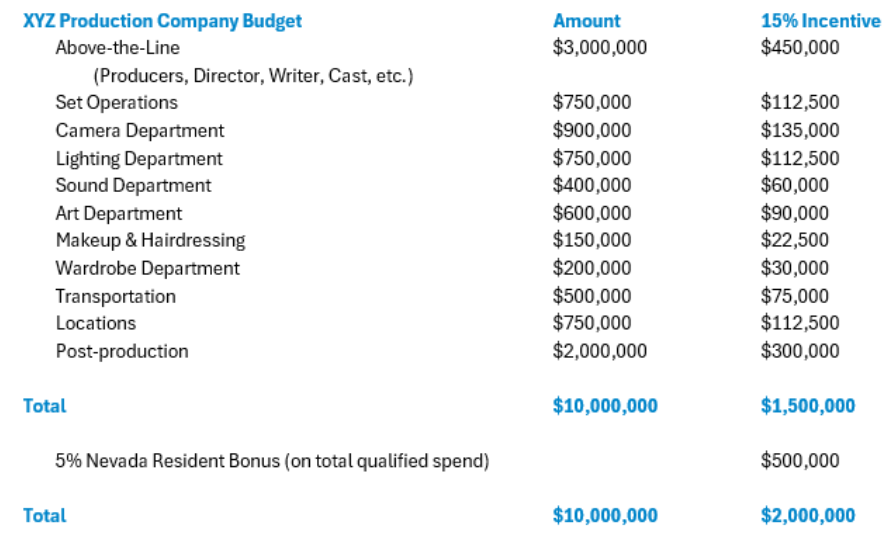

For instance, hypothetical XYZ Production Company spent $10,000,000 by filming a television series in Las Vegas. The production hired Nevada residents to account for over 50% of their below-the-line crew, earning the 5% bonus. Most of their filming days were in Clark County, so they did not qualify for the rural county bonus.

These costs are subject to standard Nevada taxes, such as sales and use for the purchases and rentals of goods, modified business tax on employee wages, lodging tax on hotel room nights and the short term lessor fee on car rentals. The Nevada Revised Statutes defines the types of costs that are considered qualified and credits are only awarded after an audit is performed by an independent Certified Public Accountant to determine that the costs are verified, reasonable and customary.

Based on the audited costs, the transferable tax credit is calculated and a certificate is issued in the amount earned.

In this example, the $10,000,000 spent on Nevada qualified costs earned a $2,000,000 transferable tax credit.

How do the tax credits work?

When a tax credit certificate is issued, it expires four years after the date of issuance and can only be applied toward these Nevada tax types specified by law:

- Gaming license fee per NRS 463.370

- Insurance premium tax per NRS 680B

- Financial institution tax per NRS 363A

- Modified business tax per NRS 363B

Of these applicable taxes, the only tax type that a production is able to incur is the modified business tax, which is a payroll tax the production can owe on wages paid to employees. In most cases, the production will prioritize monetizing the credit quickly by selling it to a Nevada business that can use it. These tax types are due quarterly or monthly, creating a year-round marketplace for their use.

This transaction is usually sold at a discounted rate, with the buyer of the credit paying less than its face value. Continuing the hypothetical scenario, XYZ Production Company has earned a $2,000,000 transferable tax credit by paying wages to Nevada cast and crew and making purchases and rentals from Nevada businesses. The production company has not incurred a $2,000,000 tax liability in one of the allowable tax types, so it finds a Nevada business that has. This can be done as a direct transaction between the production company and the buyer or through a broker. A broker is someone who works with the buyers and sellers of credits, sometimes helping to identify potential buyers, and managing the term agreements for each party, usually for a commission fee.

The production company and the buyer will negotiate the terms of the transfer, including the amount the Nevada business will pay for the credit. In the hypothetical scenario, ABC Casino has agreed to pay XYZ Production Company $1,800,000 for the credit. This is considered a private transaction between two entities and once the terms are negotiated, both parties will complete a transfer form with the State effectively transferring the ownership of the credit from the production company who earned it to the Nevada business who purchased it.

The form is filed with either the Department of Taxation (for modified business, insurance premium or financial institution taxes) or the Gaming Control Board (for gaming taxes) to redeem the credit from the Nevada taxpayer who purchased it. Continuing with the example, ABC Casino has accrued a tax liability of $2,500,000 for the month of June. When they pay their tax bill to the Gaming Control Board, they can submit the $2,000,000 credit along with a payment of $500,000 to fulfill their tax liability.

In this case, ABC Casino has effectively saved $200,000 on their tax bill (though they owed $2,500,000) they paid $1,800,000 to XYZ Production Company and $500,000 to the Gaming Control Board, fulfilling their tax liability for a total of $2,300,000 out of pocket.

XYZ Production Company has received $1,800,000 for spending $10,000,000 on qualified costs in Nevada, making it more cost effective to film their production in Nevada than in a region that does not offer an incentive for filmmakers.

What’s the cost of transferable tax credits?

Returning to the hypothetical scenario, the State of Nevada issued a tax bill to ABC Casino in the amount of $2,500,000, but received a $2,000,000 tax credit certificate and $500,000 as payment. The $500,000 is processed into the state’s coffers, while the $2,000,000 tax credit is entered as negative revenue on the state’s balance sheet. The allocation for this credit comes from the $10,000,000 in annual funding for the film tax incentive program.

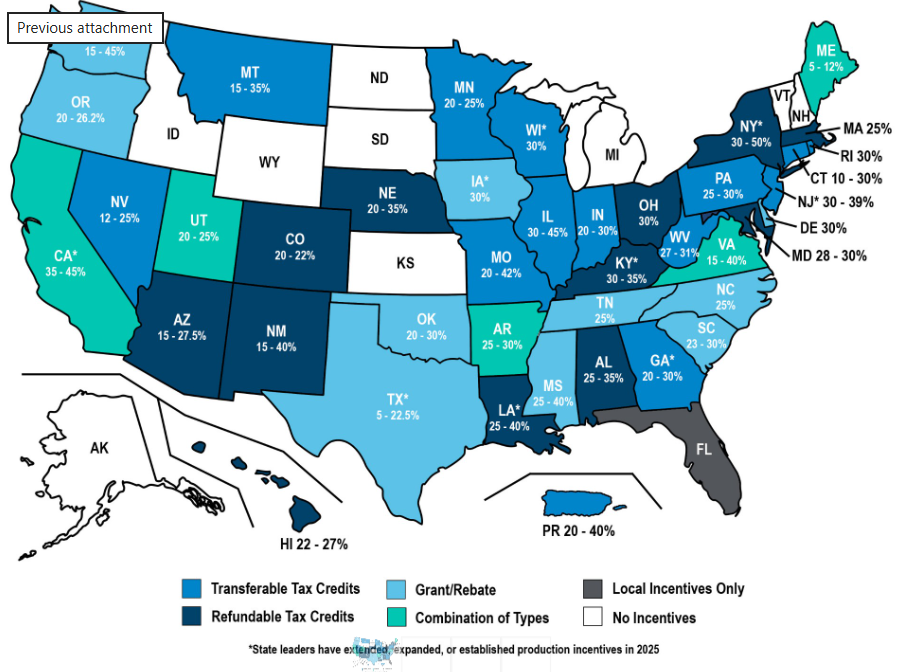

Do other regions have film incentive programs?

Most U.S. states and many territories worldwide offer a film incentive program. Currently, there are around 120 programs offered from various regions globally, including countries, states, counties and cities. The types of incentives available include grants or rebates, refundable tax credits, and transferable tax credits. The programs also vary in the incentive rates offered, the expenses that qualify, and annual funding levels available.

By offering film incentive programs, regions can drive economic impact through job creation and direct local spending. According to a study published in 2025 by the Motion Picture Association, the American film and television industry supports 2.32 million jobs, pays out $229 billion in total wages, and comprises more than 122,000 businesses. MPA member companies also made $21 billion in payments to over 194,000 local businesses. Incentive programs drive a greater market share of this spending and job creation to their regions.

Nevada’s annual funding of $10,000,000 and 15% base rate is considered low compared to the programs of other regions. For instance, the state of Georgia offers a 20% base rate plus 10% promotional credit for including the Georgia peach logo, with most productions qualifying for the 30% rate. Georgia’s funding for the program remains uncapped, with the state able to issue credits to all productions that qualify. In recent years, that has attracted over $4 billion in annual production spending.

Outside of the U.S., the United Kingdom remains a popular filming destination that offers a refundable credit to qualified productions. According to the British Film Institute, the U.K. reached £5.6 billion ($6.9 billion) in production spending in 2024. Other European countries, including Spain, Hungary and Ireland, continue to attract a large number of American productions to film in their countries through their film incentive programs.